Many business owners were hit hard during the global pandemic. Smart business owners began to reflect on what would happen to their businesses, families, and communities if they died or became disabled. Though it’s been stressful and many times felt overwhelming, having an estate plan for your business can ease some of that anxiety. You should have an estate plan to ensure your family is taken care of and part of that estate plan should be what happens to your business.

Small business owner estate planning

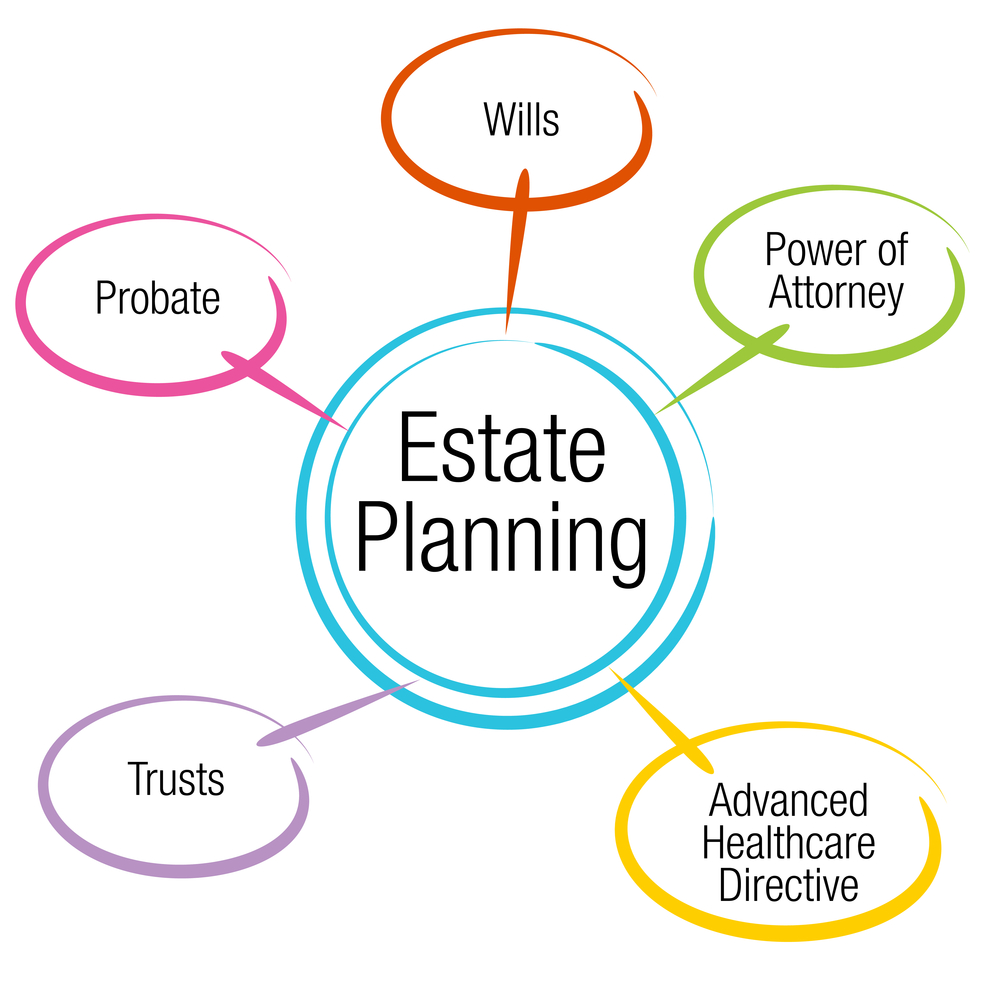

The framework for your estate plan is comprised of several documents:

- Will. A will divides your personal and business assets among specified beneficiaries. It includes designating a representative to ensure distribution is carried out according to your wishes.

- Power of attorney. The power of attorney designates someone to manage your affairs if you become incapacitated. It allows business continuity even if you are unavailable or not conscious.

- Healthcare directive. Someone you trust should have your healthcare directive and be empowered to make healthcare decisions for you if you are incapacitated.

- Trusts and FLPs. Trusts and family limited partnerships (FLPs) remove assets from your taxable estate and provide access to business funds without going through probate.

- Succession plans and buy/sell agreements. A succession plan outlines how the business will move forward in your absence and/or how it should be prepared for sale. If you have business partners, you should have buy/sell agreements in place to cover any contingencies for surviving partners.

Here’s why business estate planning is important

Business estate plans ensure that someone you trust provides continuity for your business if you cannot be present. If something happens to you, the stakeholders in your business—your family, community, employees, partners, suppliers, and shareholders—will continue to get the service and support your business provides.

Small businesses can have a big impact on these stakeholders. You worked hard to gain their trust and respect and build your business’ reputation. Without proper planning, that reputation can be put in jeopardy in an instant.

Your business is probably a large percentage of your net worth. If something were to happen to you, your family may not have access to these assets and could quickly fall into a spiral of debt.

8 steps for small business estate planning

Because Michigan probate court will not distribute your assets as you want, here is how you can define your wishes for the business:

- Create a basic estate plan and will. As mentioned above a will and some basic documents form the foundation for business estate planning. A will designates how your business should be divided. A power of attorney designates who will manage your business if you are not able to do so. A healthcare directive designates who will make healthcare decisions if you cannot.

- Create a tax plan. Tax laws can change frequently. Estate taxes and inheritance taxes can be mitigated with proper tax planning. You should review the tax implications of distributions made from retirement and other pre-tax investment and savings accounts.

- Determine if your business assets will remain in your family. Your children may or may not want to become part of or inherit your business. It’s important that you create a balance in your business estate plan that avoids future sibling fights that could have a detrimental impact on your business and your family.

- Create and review buy-sell agreements. If your business has co-owners, you need to specify who can buy shares of the business, under what circumstances, and at what price.

- Obtain life and disability insurance policies. Life insurance can guarantee an income to keep your company operating. Disability insurance also provides an income if you are incapacitated. You’ll need to buy two kinds of life and disability insurance plans – one with your family as a beneficiary and the other with your business as the beneficiary.

- Invest time in succession and continuity planning. Succession planning is essential to keep your business running. It should be an essential element of your business plan and estate plan. It provides a good opportunity to identify key staff members and training opportunities.

- Be sure your family and business partners are aware of your business estate plan. Though they may be difficult conversations to have, talking through your plan can avoid contact later on. Although they may not agree with everything in the plan, this is an opportunity to set expectations and avoid conflicts after you are gone.

- Update your plan regularly. Tax laws and business environments change over time. You may even change your mind because your family circumstances have changed. So, it’s a good idea to review your business estate plan every two to three years.

Put together a small business estate plan that fits your needs

Your business estate plan should be an essential part of your business operations. The Estate Planning Law Firm provides this online tool to help you create a customized business estate plan that’s right for you, your business, and your family. Our estate planning packages range from $99 to $1,099. They are crafted by our attorneys and customized by you. Take the quiz on our website and find the estate planning package that fits your business and your life.

It just takes three steps:

- Choose a package

- Answer a few simple questions

- Rest assured that your business and assets are protected

")

Not Sure Where to Start?

Not Sure Where to Start?

Not Sure Where to Start?

Take Our Quiz to Determine the Right Package for You

")