Most of us avoid thinking about our own deaths. Consequently, we are resistant to any mention of estate planning. Yet planning for the preservation, management, and distribution of assets in the event of death or disability is essential to securing your legacy and your family’s future stability. It’s not just an issue of who gets Aunt Maggie’s Christmas pin collection. Estate planning is not just an issue for the super-rich. Unfortunately, about two-thirds of Americans die without a will, adding to the confusion and stress of losing a loved one. Now is the time to begin the process of estate planning.

The right law firm will guide you through this difficult yet essential process with experience, a thorough understanding of trusts and estates law, and a lot of compassion. And the right law firm for affordable, no-frills estate planning is The Estate Planning Law Firm. Let us guide you through a fuller understanding of the vocabulary and process of devising a will and inclusive estate plan.

Estate Planning Basics

Estate planning, like many areas of the law, has a unique vocabulary and a list of possible documents to serve your interests.

What is Estate Planning? Estate planning is a careful and thoughtful process that anticipates the transfer of property upon death or disability that involves family goals and composition, tax liability, business succession, and continuing to provide for your spouse and children. Estate planning creates a will and sometimes trust agreements, along with a series of necessary documents to help your loved ones make end-of-life decisions on your behalf.

Estate planning requires a thorough inventory of assets and liabilities:

- real property: house, condominium, cooperative, or land

- personal property: jewelry, art, car, boat, furniture, books, and digital assets

- business ownership

- investments, bank accounts, and pensions

- insurance policies, if any

- liabilities such as outstanding debts, notes, or mortgages

Once that inventory is complete, a plan can be developed that provides for the preservation, management, and distribution of assets with an eye toward reducing tax liability and fulfilling your individual goals. Such goals might include providing for your surviving spouse and children, charitable giving, paying for your grandchildren’s college education, or maintaining ownership of familial property.

What Are the Goals of Estate Planning? Estate planning generally involves the bequest of assets to heirs and close friends, the settlement of any taxes and debts, and determining guardianship of minor children and pets. However, each person is distinctive in the specifics of these goals. And a compassionate and thorough estate planning lawyer will help develop an individualized plan that identifies your estate planning goals and creates the documents for their implementation.

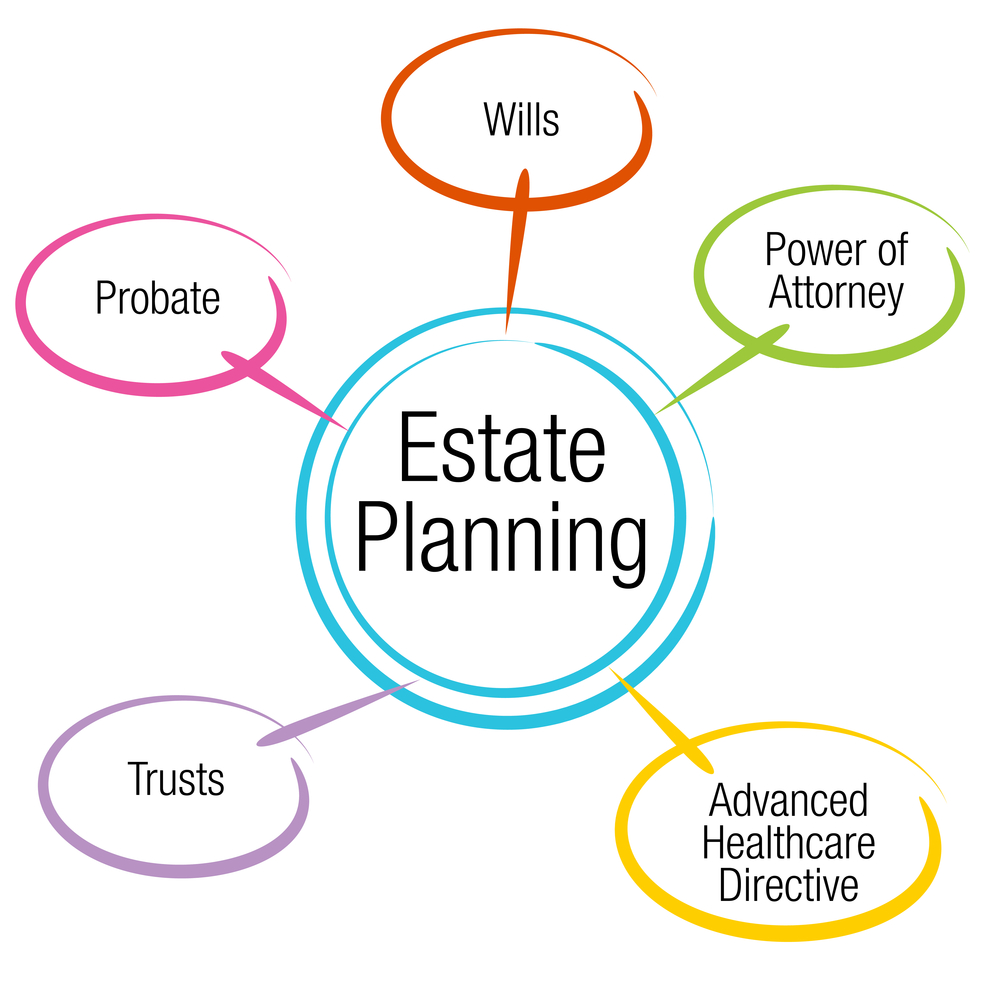

The Key Components of a Rock Solid Estate Plan: An effective and inclusive estate plan depends on your inventory of assets and liabilities and your family structure, including your spouse, children, and immediate relatives. Most estate plans involve drafting a series of documents that include the following:

- Will

- Trusts

- Power of attorney

- Advanced medical directives

Evaluating Your Estate Planning Needs

Experienced estate planning lawyers know how to break down the estate planning process into logical steps so that your financial planning is less stressful. The process begins with assessing your financial situation and anticipating future financial events.

Assessing Your Financial Situation: This first step requires an inventory of your assets—real and personal property, investments and bank accounts, and anticipated income—along with any liabilities such as loans, mortgages, and notes.

Identifying Your Goals: Estate planning can put into place structures that manage your assets after death for the benefit of your family or community. The specifics of any estate plan are unique. A thoughtful estate planning lawyer, like the professionals at The Estate Planning Law Firm, will educate you as to what estate planning can actually accomplish so that you can formulate goals that fit your financial and family situation.

Asset Protection: For individuals in high-risk occupations, such as doctors, real estate developers, investors, and the very wealthy, some states permit the creation of asset protection trusts to protect assets from creditors and to exclude assets from marital property. When permitted by state law, an asset protection trust can reduce state income taxes and remove assets from the value of an estate, further reducing tax liabilities.

Family Provisions: Marital status and whether you have children or other dependents play an important role in devising an estate plan. State law governs how marital assets are passed through a will. To protect the future financial viability of the surviving spouse, some clients opt to create a marital trust into which the estate is placed, administered by a trusted professional. Multiple marriages and children born from each union further complicate estate planning.

At different times during your life, the estate plan needs to be reassessed, especially as young children grow up, and provisions for their financial futures need to be adjusted. Obviously, a parent with young children needs to consider appointment of a suitable guardian and perhaps someone to reliably administer a family trust for the children’s benefit. Once children reach a majority, they still might not have the knowledge and experience to manage assets on their own. Children with special needs often require special needs trusts to ensure their future financial viability.

Charitable Giving: Strategic charitable giving in an estate plan can minimize taxes while supporting the religious, educational, and cultural institutions that you enjoyed during your lifetime.

Minimizing Taxes: Smart estate planning can also minimize any tax liabilities your heirs might encounter, further preserving the value of your estate.

Creating Your Will

The centerpiece of most estate plans is the will, a written document drafted according to the laws of the state in which you reside or your property is located that is signed and witnessed, which sets out your intentions for the payment of any liabilities and the distribution of assets to specific heirs, beneficiaries, trusts, and charities. Often retirement funds and investment accounts have their own named beneficiaries, which removes these assets from the scope of the will. Some real property deeds anticipate a change of ownership upon the death of an owner, and these properties are also outside the scope of the will.

Purpose of a Will: The purpose of the will is to inform the executor and heirs about the distribution of assets not covered by other legal instruments, like a trust, brokerage or bank account that has a designated beneficiary or real property deed that passes ownership to another upon your death.

Choosing an Executor: This is an essential decision assigning the task of administering the terms of the will to a specific person. The executor can be a surviving spouse, adult children, attorney, banker, or a trusted friend.

Distribution of Assets: It is up to the executor to gather the assets, pay any remaining liabilities, file the necessary state and federal tax returns, and distribute the assets according to the terms of the will.

Naming Guardians for Minor Children: When minor children might be left without a parent or parents, then an important aspect of any will is the designation of the guardian for minor children. Some estate plans separate the role of the financial manager of the assets from the responsibility of caring for the minor children.

Updating Your Will: Wills require periodic reviews in order to maintain their relevance. Federal and state estate laws change. Your marriage might end in divorce, separation, or death. You might remarry with a prenuptial to consider. Or your children might reach the age of majority. In addition, your assets can shift; you might purchase a vacation home in another state, dissolve trusts, or inherit additional assets.

Setting Up Trusts

A trust creates a way to hold and manage property for the benefit of a spouse or family members. A trust might have beneficial tax consequences and can preserve the value of assets by preventing beneficiaries from engaging in mismanagement, especially if they are young and inexperienced. A trust can also fulfill charitable goals or preserve control of a business or other assets.

Types of Trusts: Trusts vary in complexity and scope depending on the goals of the estate plan.

- Revocable Living Trusts: created during your lifetime, a revocable trust allows you to maintain control over the assets during your lifetime. However, upon death, the trust becomes irrevocable.

- Irrevocable Trusts: created either during your lifetime or at the time of your death, an irrevocable trust cannot be changed or revoked. These are often used to benefit a charity or an individual heir.

- Special Needs Trusts: created to benefit a person or persons who is ill or without the capacity to manage financial affairs.

- Charitable Trusts: created to benefit a specific charitable organization or cause. A charitable trust can operate like a private foundation without the burdensome paperwork.

Choosing a Trustee: A trustee is the person assigned to manage the assets of the trust according to the terms of the trust document. A trustee should be someone who understands finances and who understands the responsibilities of this important fiduciary role.

Benefits of Using Trusts: Trusts can be used to avoid placing assets into probate, to minimize tax consequences of the transfer of property, and to permit seamless management of assets during your lifetime and beyond. An experienced estate planning lawyer can devise trust documents when needed to fulfill your estate planning goals.

Power of Attorney

A power of attorney appoints a person to direct your health care and/or financial decisions in the event that you become incapacitated. It is automatically revoked upon your death. Then the will or trust agreements become effective.

Financial Power of Attorney: During your lifetime, if you become incapacitated, a financial or durable power of attorney will designate a person who has the legal authority to manage your assets according to the terms of the power of attorney document. Most banks and investment firms have their own forms that you will need to complete. You can limit the scope of the authority in the power of attorney document.

Medical Power of Attorney: During your lifetime, if you become incapacitated, a medical power of attorney will designate a person who has the legal authority to manage your medical care. A medical power of attorney is often paired with an advanced medical directive so that the designated person understands your wishes for extraordinary care, minimal intervention, or anything in between.

Choosing an Agent: When choosing someone to serve as your designated agent in a financial or medical power of attorney, you should choose someone whom you trust, who has the skills and temperament to make decisions on your behalf, and who can communicate well with medical and financial professionals as well as with members of the family. A spouse, an adult child, or a friend is often the designated agent. In choosing an agent for the medical power of attorney, that person should live close by with access to you and your treating doctors.

Limitations and Termination of the Power of Attorney: You can limit the authority of either a financial or medical agent within the terms of the power of attorney document. You can revoke these powers at any time while you are still competent. Both of these documents automatically expire upon your death.

Advanced Medical Directives

An advanced medical directive is also called a “living will” and provides guidance to your family as to how to deal with end-of-life decisions, such as taking extraordinary measures in the event of incapacity, inserting a feeding tube or withholding treatment, and other medical decisions. Advanced medical directives can help guide the agent designated in your medical power of attorney by letting the agent know your end-of-life wishes. These might include a Do Not Resuscitate Order (DNR) and any preferences for organ donation.

Estate Tax Planning

Currently, the federal gift and estate tax exemption is $12.92 million per person, $25.84 million for a married couple. For most clients, estate planning to minimize tax liability is not necessary. However, for high-income clients, estate planning can reduce overall federal and state estate and inheritance taxes through the use of trusts, both revocable and irrevocable, charitable giving, and gifting. However, clients of all income brackets need to be aware of gift tax limitations.

For 2023, the annual gift tax exclusion is $17,000, with $34,000 for a married couple. This means that you can gift that amount to any child, grandchild, or any other person without having to pay gift tax and without the recipient having to pay income tax on the gift.

Informed estate planning can use a variety of strategies to minimize taxation of the estate and of the beneficiaries.

Planning for Digital Assets

According to the IRS, digital assets are: “any digital representation of value which is recorded on a cryptographically secured distributed ledger or any similar technology,” as specified by the Secretary of the Treasury. Digital assets are constantly changing as this technology evolves and includes:

- Convertible virtual currency and cryptocurrency

- Stablecoins

- Non-fungible tokens (NFTs)

Like any other property, digital assets need to be included in estate planning so that they can be valued as part of the estate and can be transferred to heirs or beneficiaries.

Working With Professionals

An effective estate plan for many clients involves a team of professionals.

- Estate planning attorney

- Financial Advisor

- Tax Professional

The estate planning attorney understands the state and federal law governing the transfer of assets and the tax consequences of any transfers. The financial advisor counsels and invests assets to produce maximum income and minimize risk. And a tax professional, often an accountant, can file the necessary tax returns with the IRS and state taxing authorities.

Because federal and state laws change, and your family and financial circumstances might change, it is important to maintain relationships with each of these professionals. Once an estate plan is devised and implemented, it will need to be periodically reviewed to take full advantage of any changes to the law and to anticipate any changes in your personal life.

Affordable Legal Wills, Trusts, and Estate Planning Documents Created by Real Attorneys

Planning ahead to protect your family and loved ones can be affordable and bring peace of mind.

The Estate Planning Law Firm, PLLC, was founded with a mission to make legal matters like estate planning less intimidating and time-consuming for hard-working American families.

Our clients are teachers, firefighters, police officers, secretaries, and small business owners. We have devised a system that allows you to identify assets and liabilities and create the strategies and documents needed to implement an effective plan to protect your family and your assets.

Start protecting yourself and your loved ones today. Take our estate planning quiz to learn what you need. Then review our affordable packages –$99 to $1099 –and find the one that works for you.

")

Not Sure Where to Start?

Not Sure Where to Start?

Not Sure Where to Start?

Take Our Quiz to Determine the Right Package for You

")