The Estate planning process can be described as a way to make a solid plan with regard to the distribution of your assets after death. This sounds morbid, but it is the only way to ensure your assets and properties are distributed according to your wishes. Usually, this process is done with the guidance and advice of an attorney with the goal of ensuring intended beneficiaries and heirs receive assets in a way to manage and reduces estate and gift taxes.

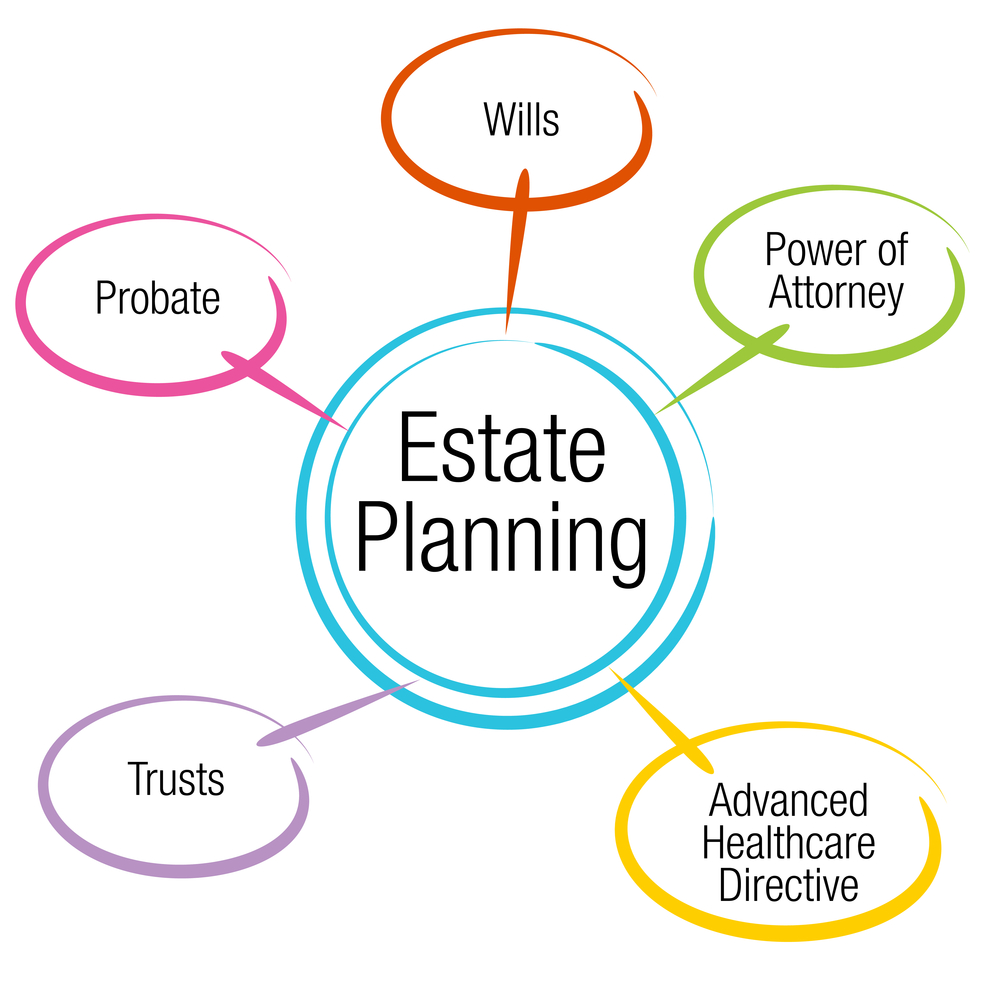

To ensure the proposed testamentary disposition is in line with your wishes, you must provide instructions tailored to whom you want to receive something, what you want them to receive, and when they receive it. In other words, the instructions must be as detailed as they can be to avoid confusion as to dispositions or bequests to beneficiaries. However, estate planning is more than just planning on whom, what, and when to receive a bequest. It should extensively include the following:

- Instructions for your health and finances if you become incapacitated before death.

- Arrangements for life insurance to provide for your family after death.

- Name a guardian for minor children’s care.

- Provide for family members with special needs.

- Provide for family members who may be careless with money or who may need protection from creditors.

- Minimize estate and gift taxes and court filing fees, which may affect the funding and administration of a living trust or update the designation of a beneficiary.

Importantly, the estate planning process is an ongoing process. Also, there is the need for constant review and updating of your estate plan, as changes can occur in financial circumstances and relevant laws as they change from time to time.

Why Estate Planning is Important

Enrolling in an estate plan is not only for a certain group of people (60+). In other words, estate planning is not simply for retirees alone, although it is normal for persons within that bracket to think of it. Unfortunately, we live in a world where it is impossible to predict how long one can live or foresee an illness happening to them. Thus, it is imperative to consider having an estate plan in place for your family and loved ones a little earlier before retirement.

People tend to make the mistake of not considering estate planning at all. This is commonly attributed to the following reasons: busy, too early to be thinking of that, not owning enough, not old enough or simply don’t know where to start, etc. These reasons are valid, depending on how you spin it. However, life doesn’t always go as planned the way we intend. Simply put, you do not want your family to go through a tedious process of picking the pieces with regard to any assets or properties that you may have if premature death befalls.

Not having an Estate Plan in place will lead to the State creating one for you. Now, that’s something you may not necessarily want, especially if you have a disability or are incapacitated. The court will supervise and control your assets as they fit using a conservator or guardian, which can be an expensive and time-consuming process. Further, if you die without an estate plan, any assets you own will be distributed by the court in accordance with the state’s intestate laws through probate. This is far from an ideal situation, especially if you are married with children. Your spouse and children (including adopted and children from a prior marriage) will each receive equal shares of your estate. Meaning your spouse will be entitled to a fraction of your estate via the elective share statute, which may not be enough. If you have minor children, there is a good chance the court will control their inheritance.

A Will and Trust: Beginning of Estate Plan

A will usually is one of the primary testamentary documents that begin the estate plan. A will provides instructions for the distribution of assets to your intended beneficiaries, but it does not avoid probate. The assets in your estate will go through the state’s probate process before they can be distributed to intended beneficiaries per your wishes. On the other hand, it is important to note that not all assets go through probate. A living trust, Jointly owned properties, retirement accounts, life insurance, and annuities are examples of assets that are not part of the will. Thus, it transfers automatically to intended beneficiaries or surviving heirs upon death. However, avoiding probate is not guaranteed. For instance, if there is no named beneficiary, the assets will have to go through probate. Also, if you name a minor as an intended beneficiary, the court will require guardianship until the child is 18 years of age or older, depending on state law.

Revocable Living Trust (combined with Pour-Over Will)

In order to avoid these situations, drafting a revocable living trust together with a pour-over will is a good option to consider. It is often highly suggested by estate planning professionals. It is preferred by many families who wish to avoid probate. Establishing and funding a revocable living trust prevents the court from controlling your assets if you become incapacitated. Another key feature of the revocable living trust is that it gives you the freedom to modify the instructions governing the administration of the trust. In other words, if you wish to change a beneficiary or bequest, you can easily make that change by yourself without needing the court’s permission to undertake such action. A pour-over will serve as a measure of backup to the revocable living trust and is a good way to transfer assets that were not funded into the trust during your lifetime to be poured over into the trust upon your death.

Moreover, trust can continue long after your death, unlike probate. Assets in your trust are managed and distributed by a trustee you selected until certain conditions are met, i.e., beneficiaries reaching the age you want them to inherit or longer to provide for loved ones with special needs. Also, a trust would help you protect your assets from beneficiaries’ creditors, irresponsible spending or even provide for future generations. An estate plan that includes a living trust and pour-over, in comparison, is not more expensive than an estate plan that only includes a will. However, you are likely to avoid fees and costs later since a funded trust avoids probate at incapacity and death.

")

Not Sure Where to Start?

Not Sure Where to Start?

Not Sure Where to Start?

Take Our Quiz to Determine the Right Package for You

")